AIPW vs. RA and IPW

Michael C. Knaus

05/25

Source:vignettes/NB_OutcomeWeights_AIPW_401k.Rmd

NB_OutcomeWeights_AIPW_401k.RmdHigh-level motivation

Augmented inverse probability weighting (AIPW) a.k.a. doubly robust estimator a.k.a. Double ML for interactive regression model has attractive theoretical properties as it fits into the Double ML universe of Chernozhukov et al. (2018). On a very high level, these properties arise from AIPW leveraging both outcome and treatment information when estimating average treatment effects. This is in contrast to (single ML) regression adjustment (RA) or inverse probability weighting (IPW), which leave treatment and outcome information on the table, respectively.

But does this matter in practice? The outcome weights derived in Knaus (2024) allow to compare the three estimators in an task familiar to many practitioners: covariate balancing.

Comparison in the 401(k) data

First, we load packages and set the seed.

if (!require("hdm")) install.packages("hdm", dependencies = TRUE); library(hdm)

if (!require("cobalt")) install.packages("cobalt", dependencies = TRUE); library(cobalt)

if (!require("viridis")) install.packages("viridis", dependencies = TRUE); library(viridis)

if (!require("OutcomeWeights")) install.packages("OutcomeWeights", dependencies = TRUE); library(OutcomeWeights)

set.seed(1234)Next, we load the 401(k) data of the hdm package.

However, you can adapt the following code chunk to load any suitable

data of your choice. Just make sure to call the outcome Y,

the treatment D and covariates X. The rest of

the notebook should then run without further modifications.

data(pension) # Find variable description if you type ?pension in console

# Treatment

D = pension$p401

# Outcome

Y = pension$net_tfa

# Controls

X = model.matrix(~ 0 + age + db + educ + fsize + hown + inc + male + marr + pira + twoearn, data = pension)

var_nm = c("Age","Benefit pension","Education","Family size","Home owner","Income","Male","Married","IRA","Two earners")

colnames(X) = var_nm

N = length(Y)AIPW and its weights

In the following we run double ML with honest random forest using the

OutcomeWeights internal implementation called

dml_with_smoother() (other packages do not store the

outcome smoothers required to calculate the outcome weights).

Run AIPW:

aipw = dml_with_smoother(Y,D,X,

# progress=T, # uncomment to see progress

# tune.parameters = "all", # uncomment to tune hyperparameters

estimators = "AIPW_ATE")

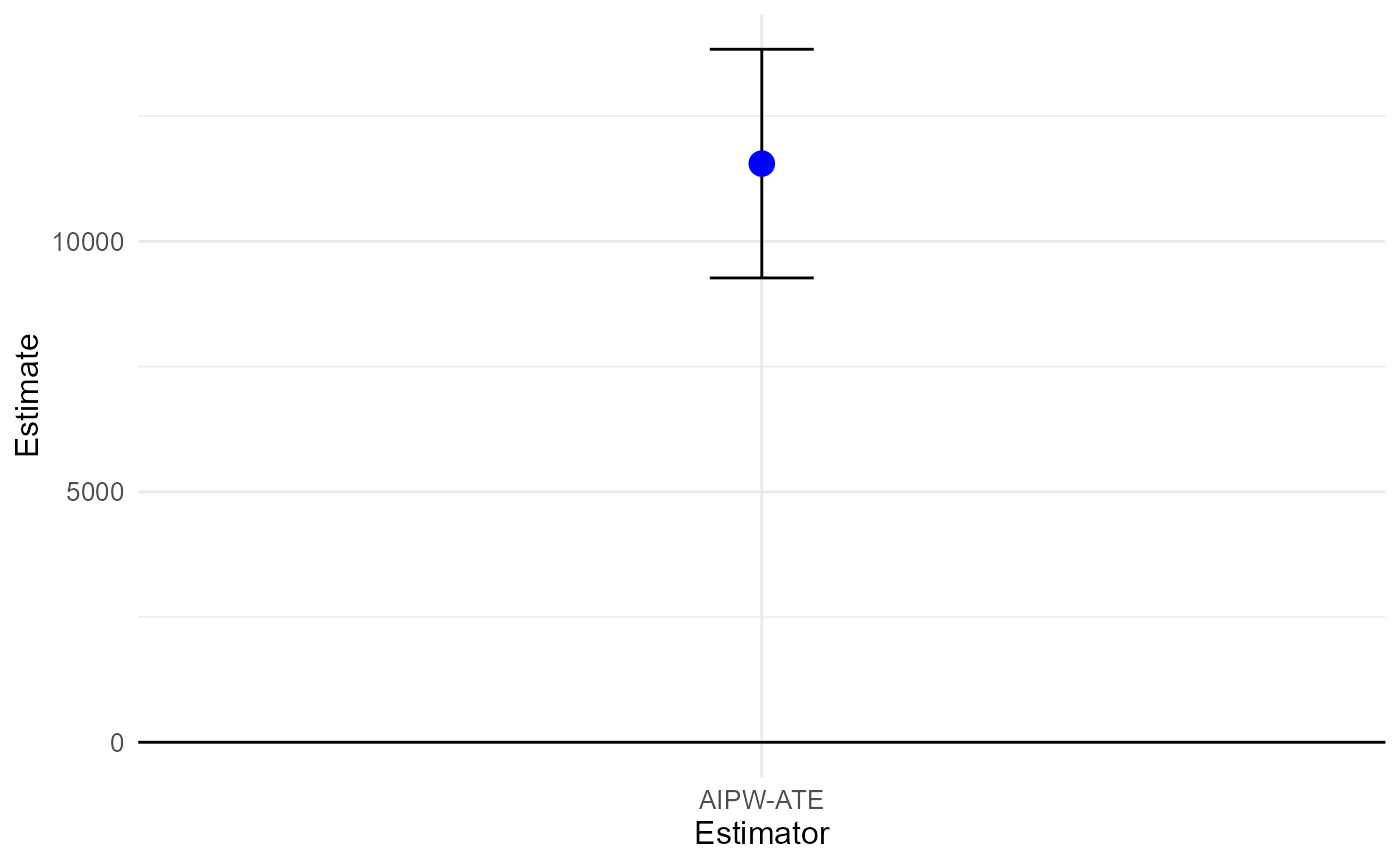

summary(aipw)## Estimate SE t p

## AIPW-ATE 11553.5 1164.5 9.9216 < 2.2e-16 ***

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

plot(aipw)

Now, we use the get_outcome_weights() method to extract

the outcome weights as described in the paper.

omega_aipw = get_outcome_weights(aipw)IPW weights

The dml_with_smoother objects also store the required

components to calculate the canonical IPW weights.

D.hat = aipw$NuPa.hat$predictions$D.hat

omega_ipw = matrix(D / D.hat - (1-D) / (1-D.hat),1) / NRA weights

The dml_with_smoother objects also store the required

components to get the RA weights that are rarely used but easy to

obtain.

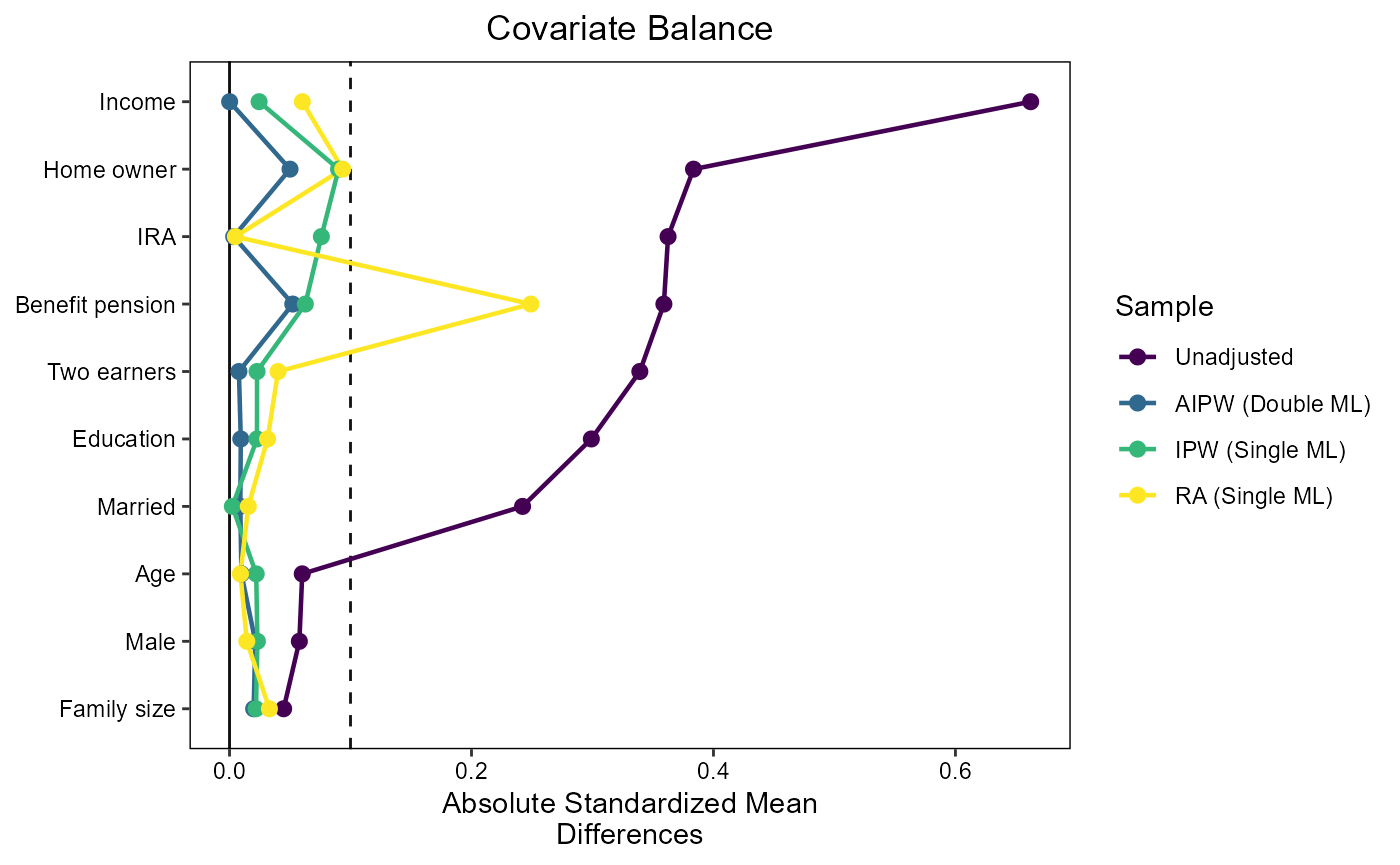

Check covariate balancing

We use the infrastructure of the cobalt

package to plot Standardized Mean Differences. To do so, we need to flip

the sign of the untreated outcome weights to make them compatible with

the cobalt framework. This is achieved by multiplying the

outcome weights by 2 \times D-1.

threshold = 0.1

love.plot(

D ~ X,

weights = list(

"AIPW (Double ML)" = as.numeric(omega_aipw$omega * (2*D-1)),

"IPW (Single ML)" = as.numeric(omega_ipw * (2*D-1)),

"RA (Single ML)" = as.numeric(omega_ra * (2*D-1))

),

thresholds = c(m = threshold),

var.order = "unadjusted",

binary = "std",

abs = TRUE,

line = TRUE,

colors = viridis(4)

)

The covariate balancing of AIPW is at least as good as the balancing of IPW and RA, and in some cases substantially better. In particular, the failure of RA to balance “Benefit pension” is striking.

Conclusion

This should only serve as a small appetizer to engage with the OutcomeWeights

package. If you run this on other data, please feel free to share your

results via any channel. In particular, if you find qualitatively

different behavior. Also please share any issues on GitHub.