Application 401(k) - average effects

Michael C. Knaus

11/24

Source:vignettes/Application_average_401k.Rmd

Application_average_401k.RmdThis notebook runs the application described in Section 5.1 of Knaus (2024). The first part replicates the results presented in the paper, the second part provides supplementary information

1. Replication of paper results

Getting started

First, load packages and set the seed:

if (!require("OutcomeWeights")) install.packages("OutcomeWeights", dependencies = TRUE); library(OutcomeWeights)

if (!require("hdm")) install.packages("hdm", dependencies = TRUE); library(hdm)

if (!require("grf")) install.packages("grf", dependencies = TRUE); library(grf)

if (!require("cobalt")) install.packages("cobalt", dependencies = TRUE); library(cobalt)

if (!require("tidyverse")) install.packages("tidyverse", dependencies = TRUE); library(tidyverse)

if (!require("viridis")) install.packages("viridis", dependencies = TRUE); library(viridis)

if (!require("gridExtra")) install.packages("gridExtra", dependencies = TRUE); library(gridExtra)

set.seed(1234)Next, load the data. Here we use the 401(k) data of the

hdm package. However, you can adapt the following code

chunk to load any suitable data of your choice. Just make sure to call

the treatment D, covariates X, and instrument

Z. The rest of the notebook should run without further

modifications.

data(pension) # Find variable description if you type ?pension in console

# Treatment

D = pension$p401

# Instrument

Z = pension$e401

# Outcome

Y = pension$net_tfa

# Controls

X = model.matrix(~ 0 + age + db + educ + fsize + hown + inc + male + marr + pira + twoearn, data = pension)

var_nm = c("Age","Benefit pension","Education","Family size","Home owner","Income","Male","Married","IRA","Two earners")

colnames(X) = var_nmRun Double ML

In the following we run double ML with default honest random forest

(tuning only increases running time without changing the insights in

this application). As standard implementations do currently not allow to

extract the outcome smoother matrices, the OutcomeWeights

package comes with a tailored internal implementation called

dml_with_smoother(), which is used in the following.

2-folds

First, we run all estimators with 2-fold cross-fitting:

# 2 folds

dml_2f = dml_with_smoother(Y,D,X,Z,

n_cf_folds = 2)

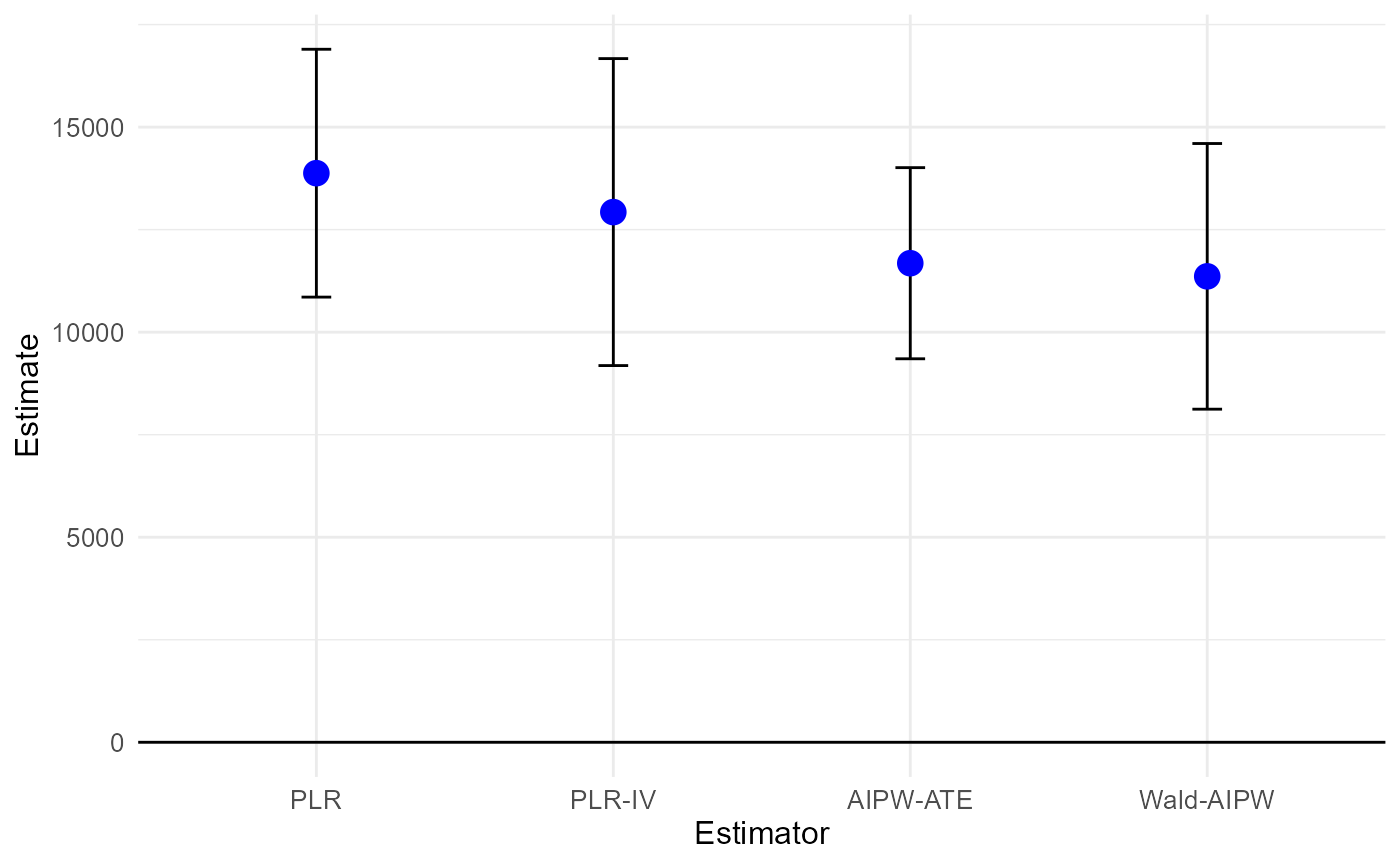

results_dml_2f = summary(dml_2f)## Estimate SE t p

## PLR 13876.4 1541.5 9.0019 < 2.2e-16 ***

## PLR-IV 12927.8 1909.3 6.7710 1.352e-11 ***

## AIPW-ATE 11681.1 1188.8 9.8258 < 2.2e-16 ***

## Wald-AIPW 11360.9 1652.3 6.8757 6.539e-12 ***

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

plot(dml_2f)

Now, we use the get_outcome_weights() method to extract

the outcome weights as described in the paper. To illustrate that the

algebraic results provided in the paper are indeed numerical

equivalences and no approximations, we check whether the weights

multiplied by the outcome vector reproduces the conventionally generated

point estimates.

omega_dml_2f = get_outcome_weights(dml_2f)

cat("ω'Y replicates point etimates?",

all.equal(as.numeric(omega_dml_2f$omega %*% Y),

as.numeric(results_dml_2f[,1])

))## ω'Y replicates point etimates? TRUE5-fold

Run double ML also with 5-fold cross-fitting:

# 5 folds

dml_5f = dml_with_smoother(Y,D,X,Z,

n_cf_folds = 5)

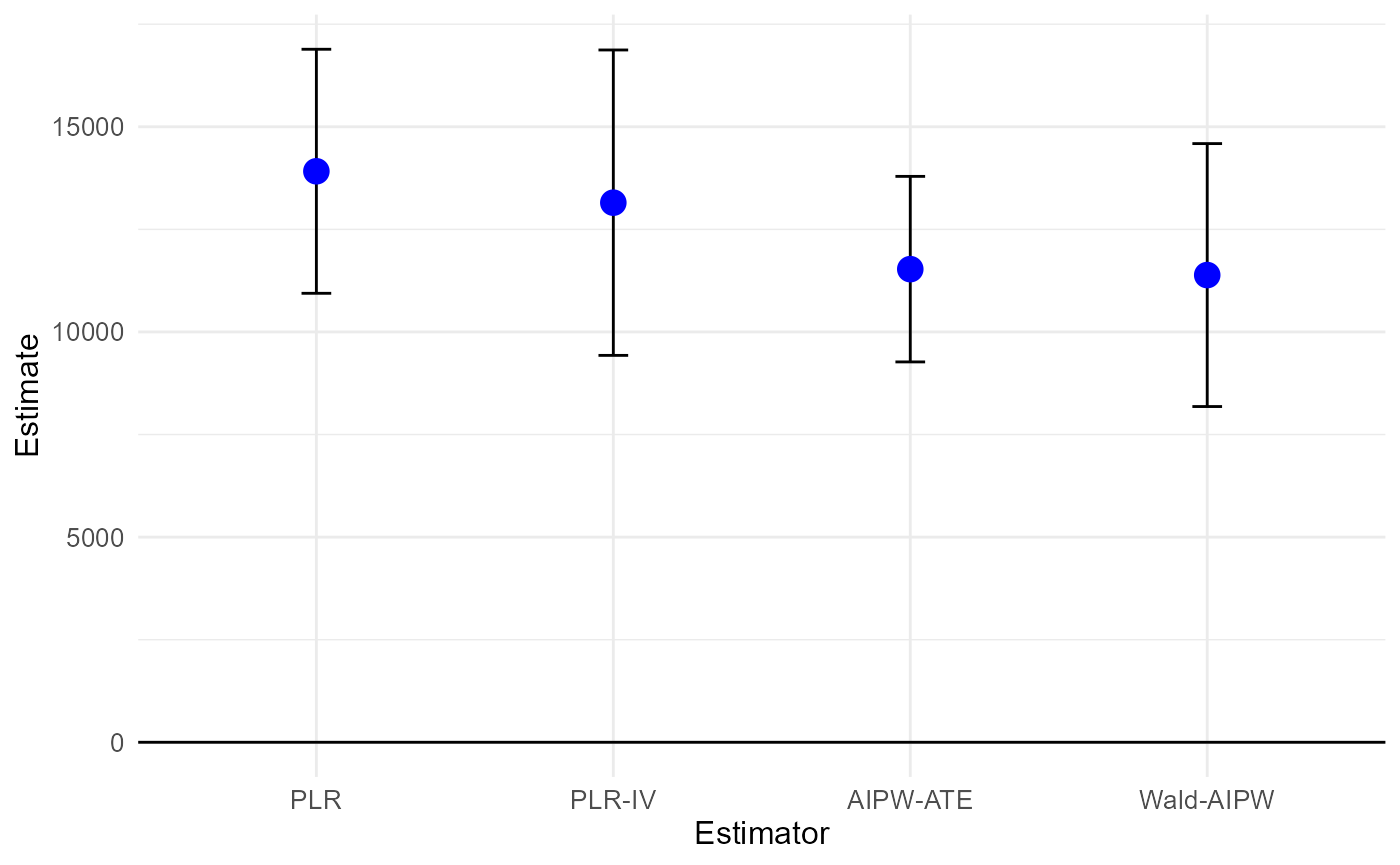

results_dml_5f = summary(dml_5f)## Estimate SE t p

## PLR 13915.5 1517.0 9.1728 < 2.2e-16 ***

## PLR-IV 13150.3 1898.5 6.9266 4.579e-12 ***

## AIPW-ATE 11530.5 1153.4 9.9972 < 2.2e-16 ***

## Wald-AIPW 11386.1 1634.5 6.9659 3.470e-12 ***

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

plot(dml_5f)

extract the weights and confirm numerical equivalence:

omega_dml_5f = get_outcome_weights(dml_5f)

cat("ω'Y replicates point etimates?",

all.equal(as.numeric(omega_dml_5f$omega %*% Y),

as.numeric(results_dml_5f[,1])

))## ω'Y replicates point etimates? TRUECheck covariate balancing

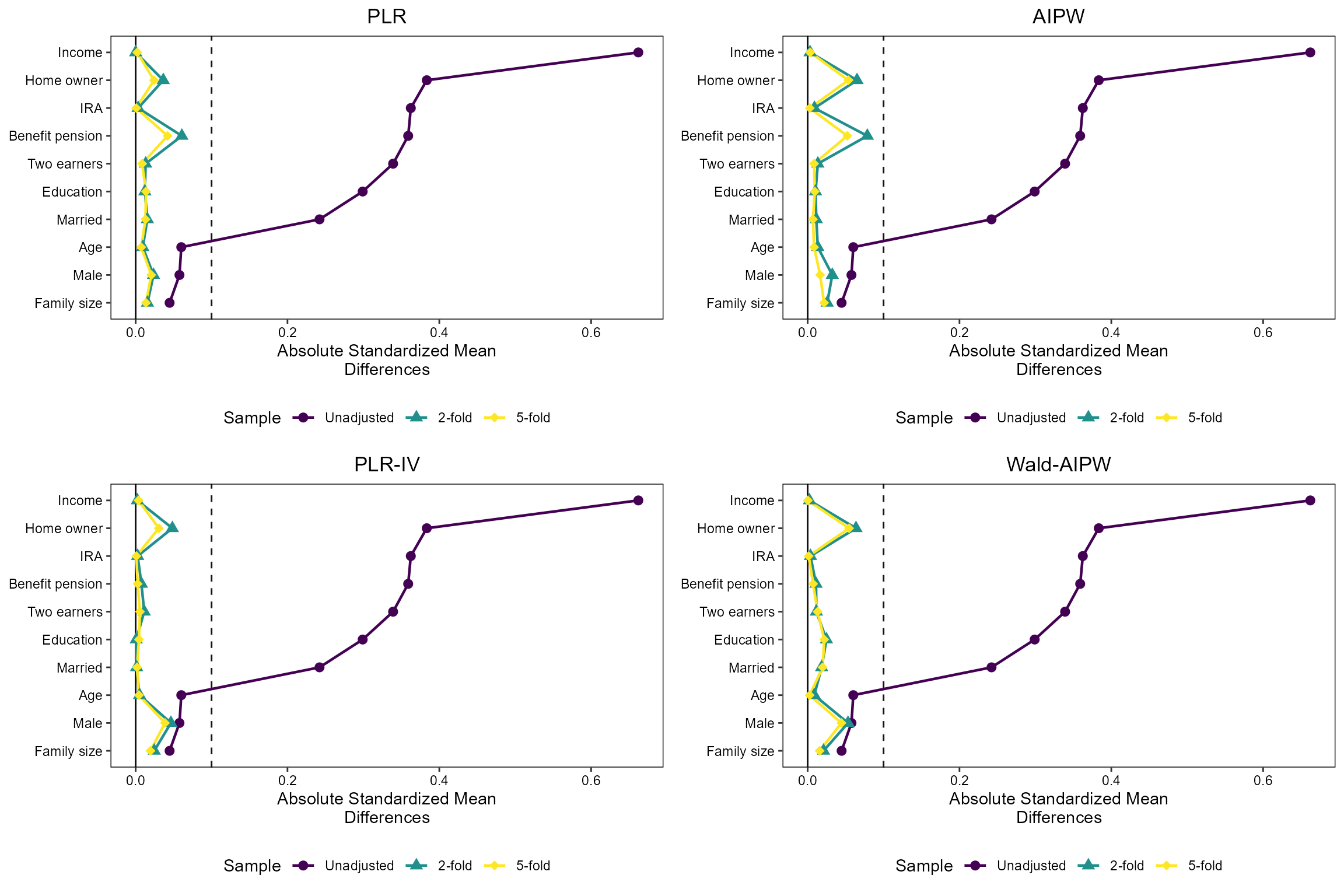

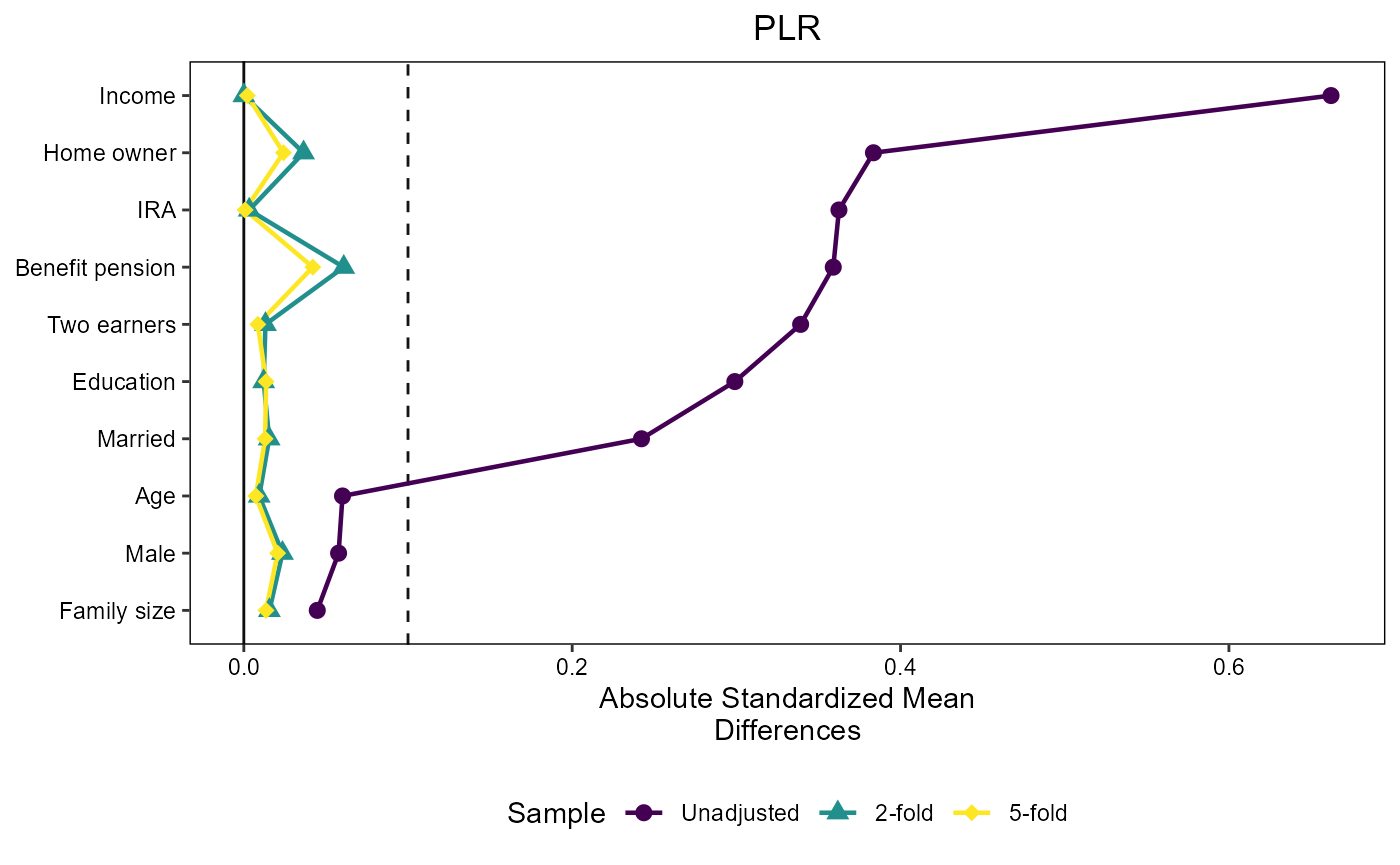

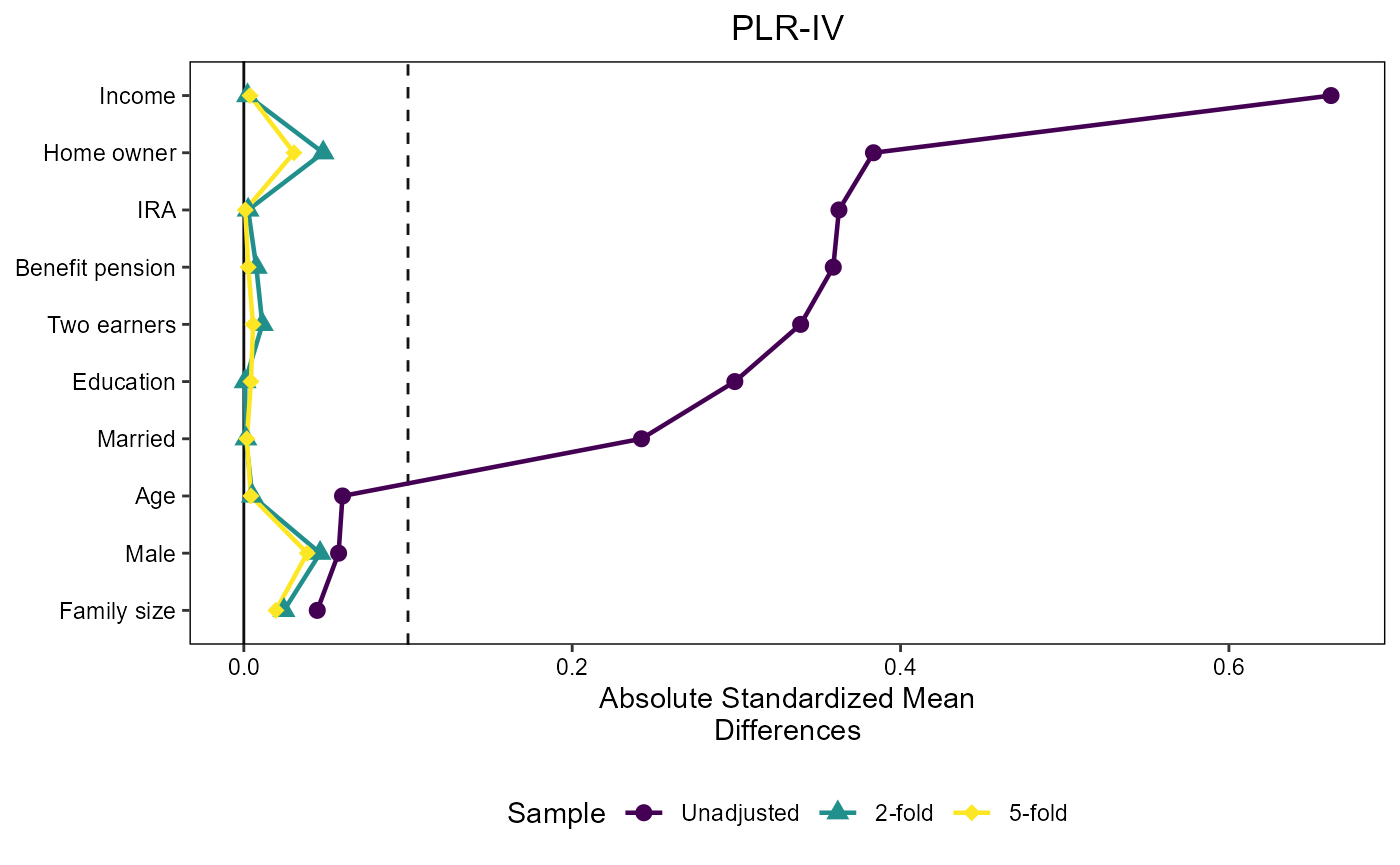

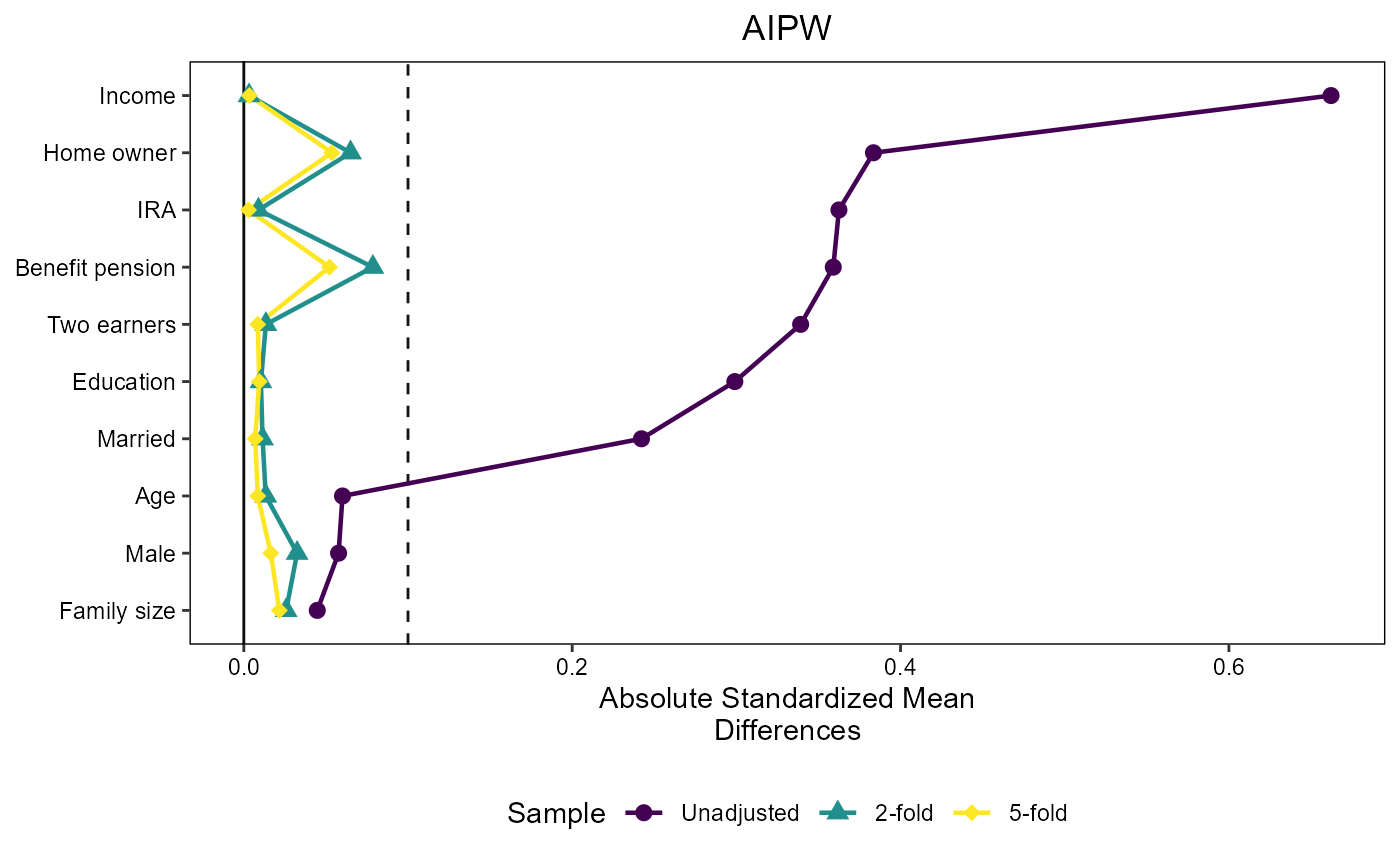

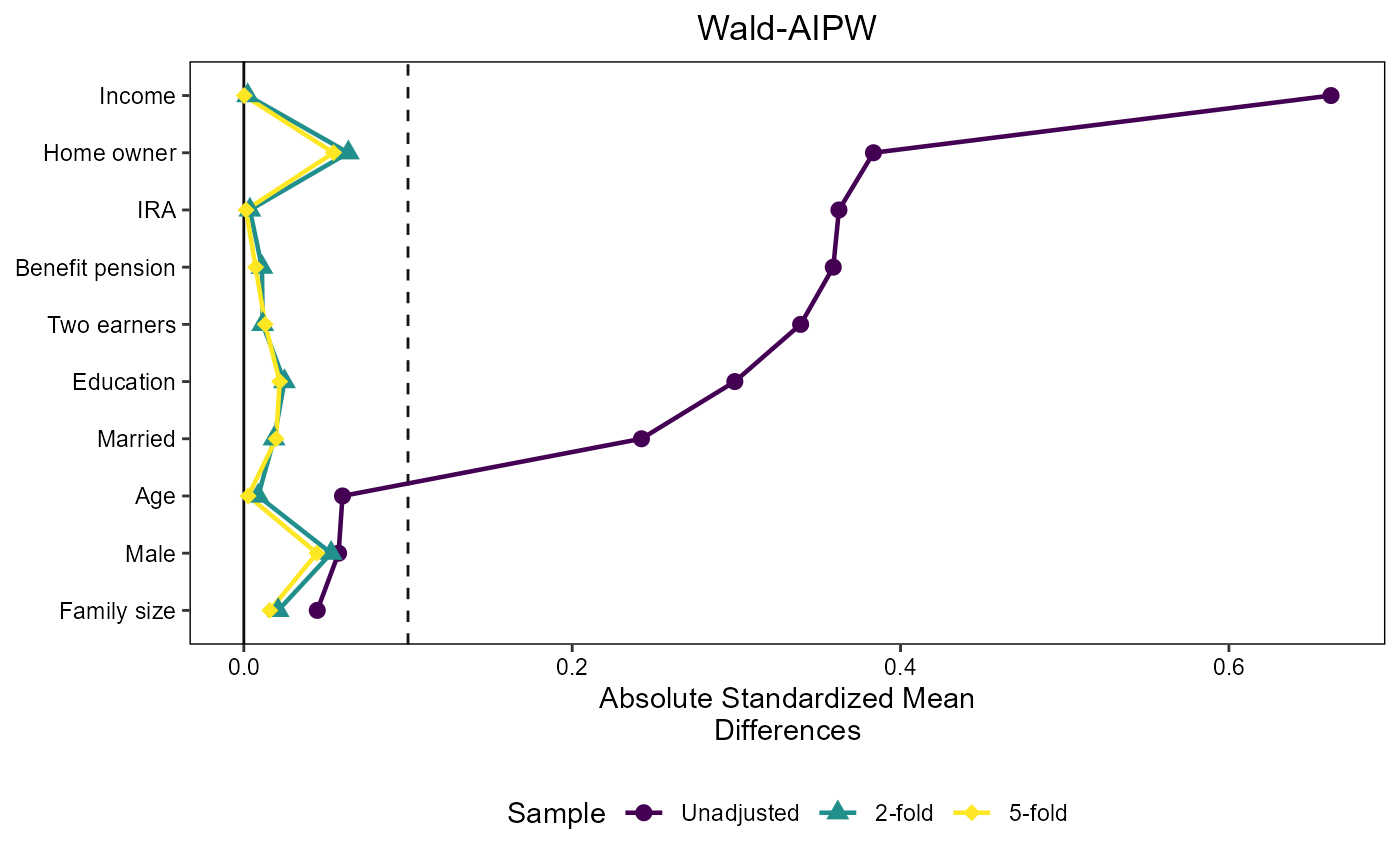

We use the infrastructure of the cobalt package to plot

Standardized Mean Differences where we need to flip the sign of the

untreated outcome weights to make them compatible with the package

framework. This is achieved by multiplying the outcome weights by 2 \times D-1:

threshold = 0.1

create_love_plot = function(title, index) {

love.plot(

D ~ X,

weights = list(

"2-fold" = omega_dml_2f$omega[index, ] * (2*D-1),

"5-fold" = omega_dml_5f$omega[index, ] * (2*D-1)

),

position = "bottom",

title = title,

thresholds = c(m = threshold),

var.order = "unadjusted",

binary = "std",

abs = TRUE,

line = TRUE,

colors = viridis(3), # color-blind-friendly

shapes = c("circle", "triangle", "diamond")

)

}

# Now you can call this function for each plot:

love_plot_plr = create_love_plot("PLR", 1)

love_plot_plriv = create_love_plot("PLR-IV", 2)

love_plot_aipw = create_love_plot("AIPW", 3)

love_plot_waipw = create_love_plot("Wald-AIPW", 4)

love_plot_plr

love_plot_plriv

love_plot_aipw

love_plot_waipw

Create the combined plot that ends up in the paper as Figure 2:

figure2 = grid.arrange(

love_plot_plr, love_plot_aipw,

love_plot_plriv,love_plot_waipw,

nrow = 2

)