Application 401(k) - heterogeneous effects

Michael C. Knaus

11/24

Source:vignettes/Application_heterogeneous_401k.Rmd

Application_heterogeneous_401k.RmdThis notebook runs the application described in Section 5.2 of Knaus (2024). The first part replicates the results presented in the paper, the second part provides supplementary information

1. Replication of paper results

Getting started

First, load packages and set the seed:

if (!require("OutcomeWeights")) install.packages("OutcomeWeights", dependencies = TRUE); library(OutcomeWeights)

if (!require("hdm")) install.packages("hdm", dependencies = TRUE); library(hdm)

if (!require("grf")) install.packages("grf", dependencies = TRUE); library(grf)

if (!require("tidyverse")) install.packages("tidyverse", dependencies = TRUE); library(tidyverse)

if (!require("viridis")) install.packages("viridis", dependencies = TRUE); library(viridis)

if (!require("reshape2")) install.packages("reshape2", dependencies = TRUE); library(reshape2)

if (!require("ggridges")) install.packages("ggridges", dependencies = TRUE); library(ggridges)

set.seed(1234)Next, load the data. Here we use the 401(k) data of the

hdm package. However, you can adapt the following code

chunk to load any suitable data of your choice. Just make sure to call

the treatment D, covariates X, and instrument

Z. The rest of the notebook should run without further

modifications.

data(pension) # Find variable description if you type ?pension in console

# Treatment

D = pension$p401

# Instrument

Z = pension$e401

# Outcome

Y = pension$net_tfa

# Controls

X = model.matrix(~ 0 + age + db + educ + fsize + hown + inc + male + marr + pira + twoearn, data = pension)

var_nm = c("Age","Benefit pension","Education","Family size","Home owner","Income","Male","Married","IRA","Two earners")

colnames(X) = var_nmGet outcome model and smoother matrix

The grf package does not save the nuisance parameter

models. Thus, we could not retrieve the required smoother matrices after

running causal_forest and instrumental_forest

below. Therefore, we estimate the outcome nuisance model externally to

pass the nuisance parameters later to the functions. As described in

Section 5.2 of the paper, we run a default and a tuned version:

### Externally calculate outcome nuisance

rf_Y.hat_default = regression_forest(X,Y)

rf_Y.hat_tuned = regression_forest(X,Y,tune.parameters = "all")

Y.hat_default = predict(rf_Y.hat_default)$predictions

Y.hat_tuned = predict(rf_Y.hat_tuned)$predictionsThen, we extract the smoother matrix using

get_forest_weights():

# And get smoother matrices

S_default = get_forest_weights(rf_Y.hat_default)

S_tuned = get_forest_weights(rf_Y.hat_tuned)For illustration, check that random forest is an affine smoother by summing all smoother vectors and checking whether they sum to one:

## RF affine smoother? TRUECausal forest

Run causal forest with the externally estimated outcome nuisance:

# Run CF with the pre-specified outcome nuisance

cf_default = causal_forest(X,Y,D,Y.hat=Y.hat_default)

cf_tuned = causal_forest(X,Y,D,Y.hat=Y.hat_tuned,tune.parameters = "all")Get the out-of-bag CATEs:

Use the new get_outcome_weights() method, which requires

to pass the externally estimated outcome smoother matrix:

omega_cf_default = get_outcome_weights(cf_default, S = S_default)

omega_cf_tuned = get_outcome_weights(cf_tuned, S = S_tuned)Observe that the outcome weights recover the grf package

output:

cat("ω'Y replicates CATE point estimates (default)?",

all.equal(as.numeric(omega_cf_default$omega %*% Y),

as.numeric(cates_default)

))## ω'Y replicates CATE point estimates (default)? TRUE

cat("\nω'Y replicates CATE point estimates (tuned)?",

all.equal(as.numeric(omega_cf_tuned$omega %*% Y),

as.numeric(cates_tuned)

))##

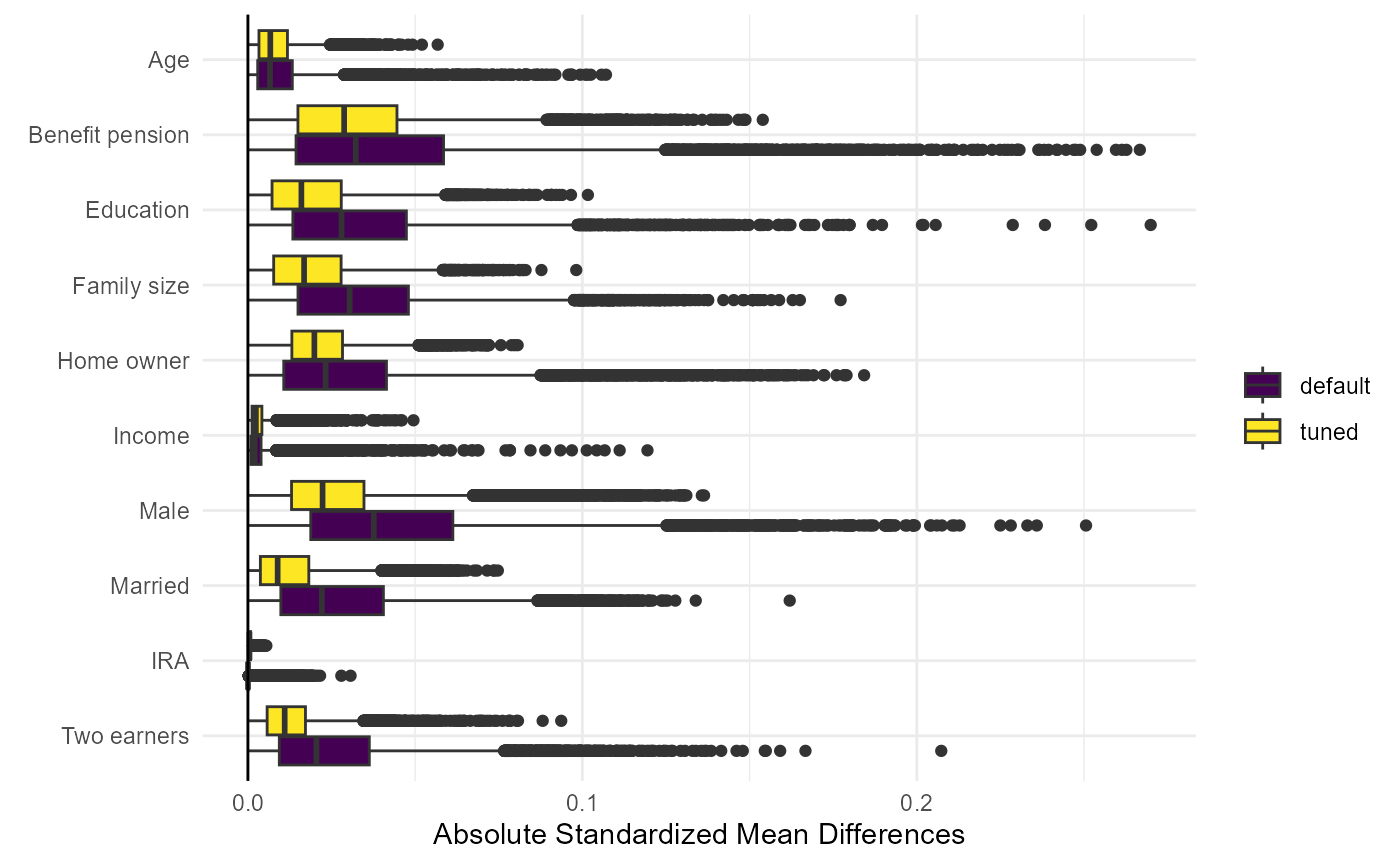

## ω'Y replicates CATE point estimates (tuned)? TRUENow calculate the absolute standardized mean differences and plot them for each CATE and variables (Figure 3 in paper):

cb_cate_default = standardized_mean_differences(X,D,omega_cf_default$omega,X)

cb_cate_tuned = standardized_mean_differences(X,D,omega_cf_tuned$omega,X)

smd_default = t(abs(cb_cate_default[,3,]))

smd_tuned = t(abs(cb_cate_tuned[,3,]))

# Melt the smd_default matrix to long format

df_default_long = melt(smd_default)

df_default_long$Group = "smd_default" # Add a group identifier

# Melt the smd_tuned matrix to long format

df_tuned_long = melt(smd_tuned)

df_tuned_long$Group = "smd_tuned" # Add a group identifier

# Combine the two data frames

df_long = rbind(df_default_long, df_tuned_long)

# Rename the columns for clarity

colnames(df_long) = c("Row", "Variable", "Value", "Group")

# Create the ggplot

figure3 = ggplot(df_long, aes(x = factor(Variable, levels = rev(unique(Variable))), y = Value, fill = Group)) +

geom_boxplot(position = position_dodge(width = 0.8)) +

labs(x = element_blank(), y = "Absolute Standardized Mean Differences") +

scale_fill_manual(values = viridis(2),

name = element_blank(),

labels = c("default", "tuned")) +

theme_minimal() +

geom_hline(yintercept = 0, linetype = "solid", color = "black") +

coord_flip()

figure3